A variance report is one of the most commonly used accounting tools. It is essentially the difference between the budgeted amount and the actual, expense or revenue.

A variance report highlights two separate values and the extent of difference between the two.

It is this variance, or the difference, that it seeks to throw light on (and eventually the triggers as well). Typically, the variance report can be created only when the actual numbers are available.

The variance can be depicted both in absolute terms as well as a percentage difference. That highlights the degree of difference and that is why it is a crucial component in many accounting practices. It brings to light an inaccurate assumption or triggers that result in the variance.

Interested in Finance?

Learn all about it in our comprehensive (and free) ebook!

The formula for variance report

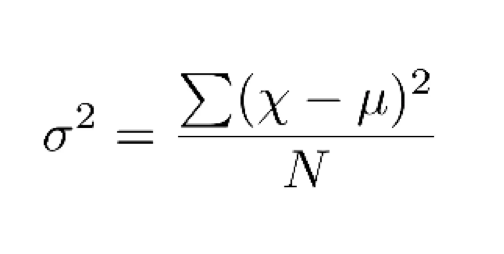

The variance report is created for all types of budgets. Typically the report is created after calculating the variance as per a strict formula. This is because the Variance comprises a key component of asset allocation. The formula for Variance is:

In this case:

- σ2 is the actual variance

- χ stands for the specific data in question

- μ is the mean of multiple data points

- N is the total number of data calculated

In case you are calculating the Variance % as a component of the Budget-Variance % = [Variance /Budget] x100

The percentage is crucial as it gives you a sense of the relative difference, and, in many cases, highlights the triggers that led to the difference.

Interested in Finance?

Learn all about it in our comprehensive (and free) ebook!

Insight into variance report

The whole concept of variance report is that of comparison. It helps in identifying the materiality of a specific budget in question. It may be surprising but the first variance report and analysis was used in ancient Egypt.

Cardinally, it is the bastion of management accountancy. This is the most important tool that managements the world over use to calibrate their company’s performance, by assessing profit and loss and paying attention to budgetary differences. Therefore, it is a tool used to enhance efficiency in a long-standing manner and sustainably over a period of time.

Bonus: Check out Finance instructor Ray Sheen's top 10 finance tips

Interpreting variance report results

The variance report is often seen as the primary tool for better controlling future costs and conditions in a meaningful way. They are the perfect representation of how independent numbers are related to one other in a bigger group.

In statistics parlance, the biggest advantage of this type of report is that it gives equal importance to all types of deviations in an analysis. Regardless of the direction of their deviation from the mean, you cannot achieve a sum zero with this kind of number reporting. As a result, you will never see a situation where you get the appearance of no deviation or variance.

That essentially means that even the smallest deviation is earmarked appropriately in the variance report results.

But that does create a small hiccup. The interpretation of the variance report is not as simple as you assumed. You need to have a proper understanding of this calculation method, the dynamics of the industry for which you are analyzing and the specific number.

Remember variance gives added weight to each of these data points and squaring them can skew the numbers in a complicated and confusing way. Most importantly, it will not serve the core purpose for which it is computed in a meaningful way.

Perhaps an example will drive home the point in a meaningful way. Let us assume that we are computing the variance report for Company X. The returns for:

- Year 1 is at 10%

- Year 2 is at 15%

- Year 3 is at -10%

The overall average for the three years is around 5%.

Now let’s say the difference the return and the average is roughly at:

- Year 1- 5%

- Year 2- 15%

- Year 3- 20%

Squaring these, you will get a deviation and variance close to 200%. Your standard deviation from this then stands at a tad lower than 15%.

Positive vs. negative variances

It is interesting to note that the variance is never unidirectional. Especially for budget variance reports, you can have both negative and positive scenarios. Essentially this is dependent on both the key calculation metrics as well as the quality of analysis. External factors like seasonal changes, for example, can play a role in it.

Positive variance

Typically a positive variance refers to favorable variances in the report that you have compiled.

It means the gains are more than anticipated and have been due to certain unexpected factors. It creates a surplus and additional gains from a variety of factors. So then the company has to get back to the drawing board and recalibrate the assets available.

It can also result in a refined asset allocation for them as well. Additionally, this can be also due to sudden unprecedented one-time windfall of some type. This can skew numbers adversely.

Negative variance

This is the exact opposite of the positive variance. This is the outcome of some unfavorable development.

The losses could have been the direct result of some sort of calculation error or even some environmental factor. For example, if you are in the cement business, the cyclical factors come to play like rains and festive demand for new houses. As a result, demand for cement is likely to spike up around then. But let’s think of the time soon after the subprime crisis, prices completely bottomed out and the demand for houses too came down. It is almost natural that the cement prices will slip as well. Therefore, a negative variance is not surprising in this circumstance.

Nevertheless, these numbers and the variance especially will give the owners a sense of the market and give them cues on how to taper down the assumptions for the following few quarters.

Common types of variances

But when you consider the variance report, it is very obvious that there are some basic parameters that keep shifting on a regular basis.

1. Price variance

In this case, as the name suggests the variance comes in the price of the material. When the actual price of the material differs significantly from the standard price you get this variance.

This is also a result of the difference in the actual output and usage levels compared to the standard ones. So, in this case, you have to keep in mind four factors:

- Actual usage. Sometimes you can get quantity discounts when you are buying larger quantities, so more materials get used to accommodate the price difference.

- The actual price being lower or higher than the standard market rate.

- The quality of the materials is also crucial. Sometimes buying lower grade or higher grade quality compared to the standard rate can be problematic too.

- The unavailability of certain products may also result in opting for another alternative. Both in terms of price and quality, it can add a different dimension to the overall variance report in a significant manner and alter the final deductions.

2. Usage variance

As the name indicates, when the usage levels are different from the standard rate, it leads to the formulation of the following report:

- Replacing the standard material with an alternative can affect usage. You may have to increase or decrease quantity as per the new requirements.

- The relative yield from the material needs to conform to expected levels. In case there is an anomaly here, it results in a variance.

- The rate of scrap from the material used can also play a crucial role in the ultimate deductions.

3. Labor variance

The labor variance refers to the cost of labor. The actual rate, in this case, at times differs significantly from the standard or assumed rate. There can again be several reasons for this making a difference in the variance report:

- If the standard rate of wage is significantly below or above the existing one.

- Actual labor hours vs. the standard labor hours can also affect both quality and efficiency. This can, in turn, have a bearing on the prices.

- Impact of special situations like strike, lockout and the like.

- Overall efficiency of the labor counts as well. If they are very efficient then, 4 laborers in 5 hours can work the same that 10 may be able to achieve in 8 hours.

4. Overhead spending variance

This refers to the overhead costs in the business. Technically it can be anytime and anything. The trick is all about incorporating the potential variables:

- Sudden one-time expenses or emergencies that have a bearing on the overall input cost.

- Potential external factors that might affect the demand for the final product.

- Labor unrest or special steps taken to offer additional financial compensation to the laborers for a specific year.

- Faulty production due to any oversight that will have to be rejected and the company has to digest the expense.

How to write a variance report

So now that you have all the elements of computing a variance report, the next step is writing it down.

The layout of the report can vary depending on how your audience wants to see the information.

The layout of the report can vary depending on how your audience wants to see the information.

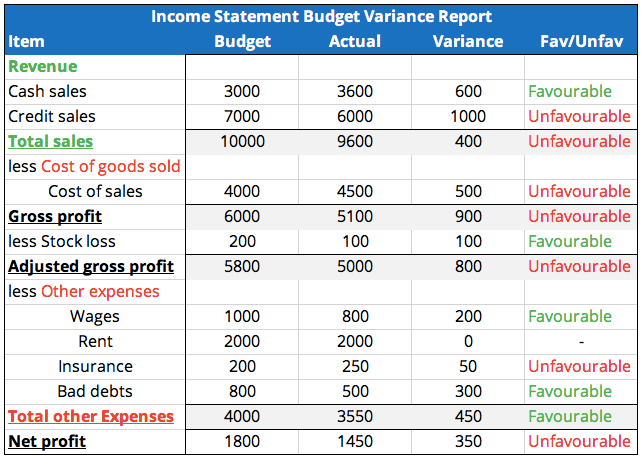

For the income statement example above, the budget for each account is listed after the account name followed by actual results. This sets the stage for the variance and then a visual favorable or unfavorable presentation. The example doesn’t show it, but variance reports can also have a column for a percentage of change to make the data even better.

Unfortunately, a variance report can’t be finalized until the actual events occur. However, a lot of work can be done beforehand by creating the template. This way turn around time once results are final will be much faster.

On the whole, most variance reports follow this strict protocol while writing it. But remember a variance report contains a lot of numbers and it is important to highlight the most relevant factors in the proper light. That will optimize its utility.

Conclusion

While variance reports can be a pain point for any professional, they are invaluable in communicating results to external stakeholders and decision-makers.

Now that you’ve mastered the basics of these reports you should be equipped to conquer your next assignment. Want to keep growing your knowledge?

Check out GoSkills Finance and Project Management courses where you can practice your new variance reporting skills.

And taking things up a notch with our guide to analysis of variance (ANOVA).